ECAN directed to pay 2.5 million in taxes, including penalties (with order)

In light of the tribunal's ruling, it appears that ECAN's attempts to evade tax obligations will prove futile. ECAN now has the option to appeal to the Supreme Court against the tribunal's decision.

KATHMANDU: The Educational Consultancy Association of Nepal (ECAN) has to pay more than two and a half million additional taxes.

The decisions rendered by the Internal Revenue Office Battisputali and the Revenue Investigation Department were affirmed by the Revenue Tribunal, mandating ECAN to remit taxes along with penalties and interest.

In light of the tribunal’s ruling, it appears that ECAN’s attempts to evade tax obligations will prove futile. ECAN now has the option to appeal to the Supreme Court against the tribunal’s decision.

However, the Supreme Court must first determine if a review of the judgment is warranted. Should the Supreme Court find no necessity for review, the ruling of the Revenue Tribunal will stand.

All three offices have concurred that ECAN has failed to fulfill tax obligations for six consecutive fiscal years.

How much tax is due for which year?

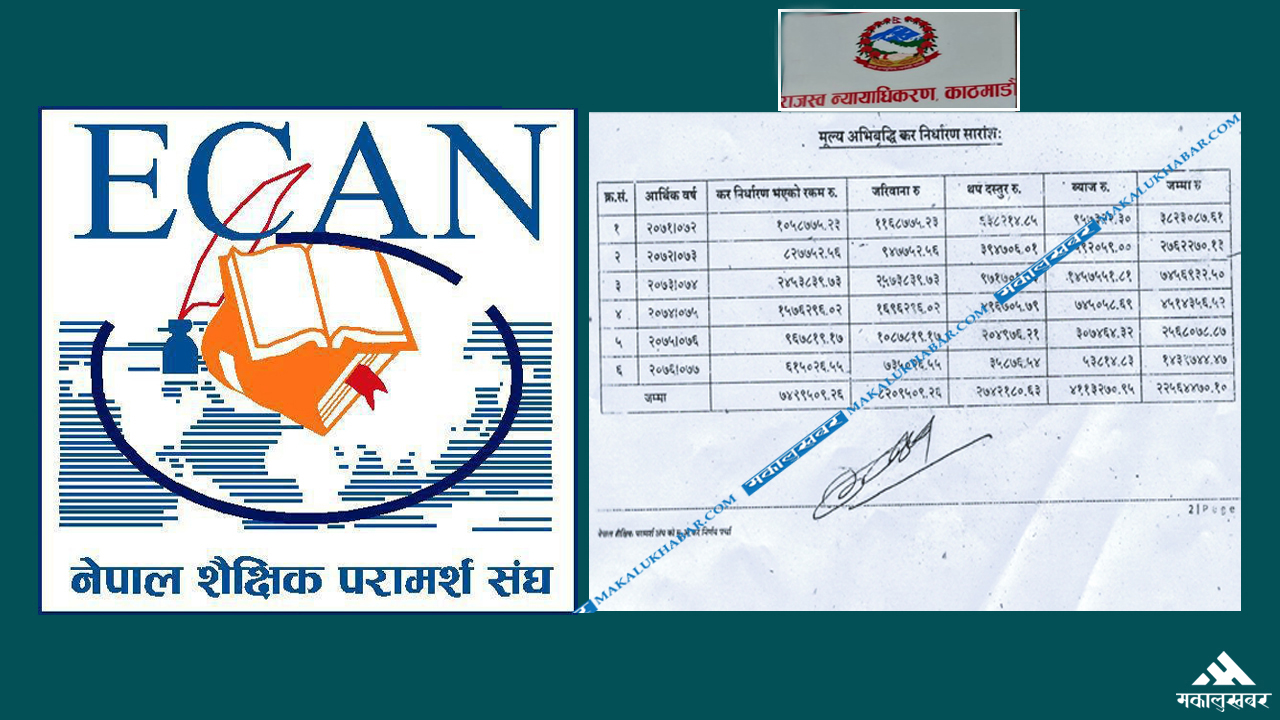

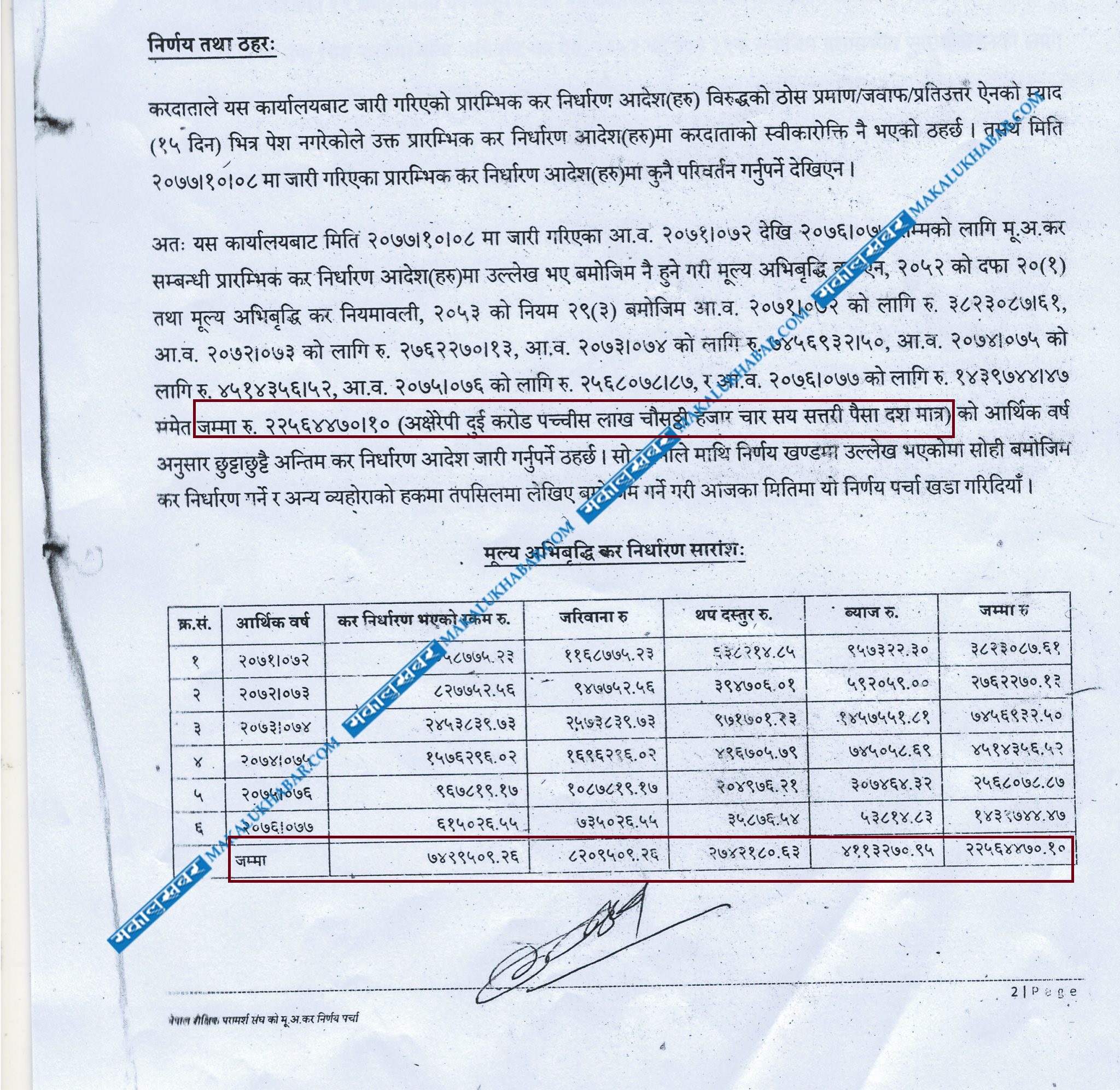

The ECAN has been directed to calculate the fee, inclusive of service tax, as per instructions from the Department of Revenue. In accordance with the decision, ECAN is mandated to set the fee at 2,25,64,470 rupees for the forthcoming six fiscal years, to be deposited from the financial year 2071/072 to 2076/077. Any attempt by ECAN to evade taxes will result in penalties, additional charges, and accrued interest.

The tax amount for these six fiscal years totals 7,499,509 rupees. Failure to report on time will incur fines, additional fees, and interest. A fine of 82 lakhs 9,509 rupees must be paid, alongside an additional fee of 27,42,180 rupees, and accrued interest amounting to 4113,270 rupees.

The highest tax submission by ECAN will be required in the financial year 2073/074. As per the tax office’s determination, a tax payment of 7456,932 rupees is stipulated solely for that fiscal year.

For the initial financial year 2071/072, 38 lakh 23 thousand 87 rupees, for 2072/073, 2762,270 rupees, and for 2074/075, 45,14,356 rupees have been earmarked. Additionally, 256,878 rupees in 2075/076 and 1439,744 rupees in 2076/077 have been allocated.

Initially, when the tax office inquired about the issue of tax evasion, ECAN failed to provide a response. Despite the preliminary tax assessment order being issued on Magh 8, 2077, the taxpayer ECAN only acknowledged it on Magh 9. However, no response was submitted within the 15-day deadline stipulated by the Act.

The Revenue Department has interpreted ECAN’s inaction as an admission of guilt. The office’s decision states, “As the taxpayer did not furnish substantial evidence against the preliminary tax assessment order issued by this office within the prescribed 15-day timeframe of the reply act, it is deemed that the aforementioned preliminary tax assessment order has been accepted. Consequently, no alterations need to be made to the preliminary tax assessment order issued on Magh 8, 2077.

These are the bases of tax assessment

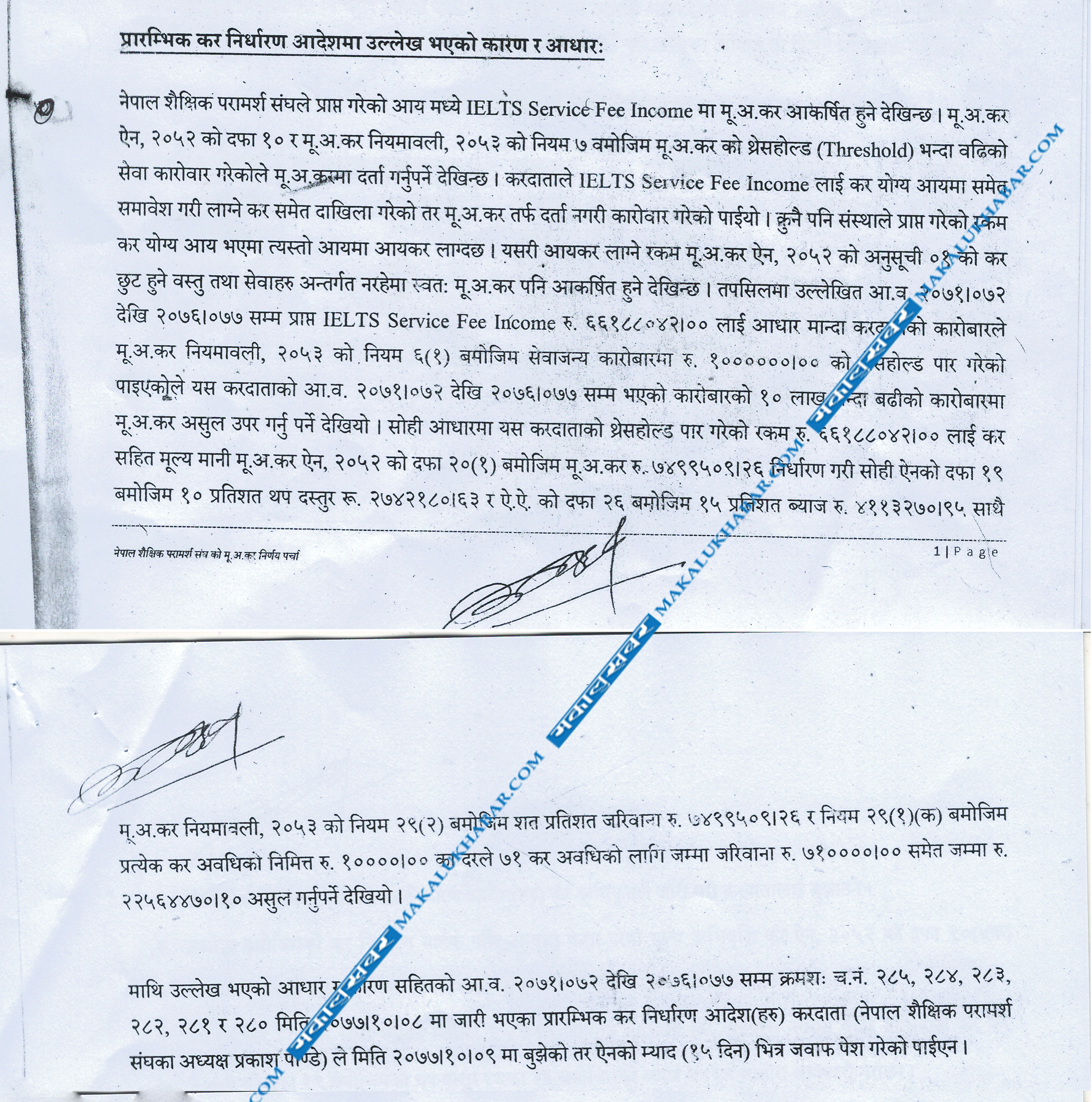

The Nepal Educational Consultancy Association has determined that value-added tax will be deducted from the oil service fee money collected. According to Section 10 of the value-added Tax Act, 2052 and Rule 7 of the value-added Tax Regulations, 2053, the tax office stated that because the service transaction is above the value-added tax threshold, it must be registered for value-added tax.

It was discovered that the taxpayer ECAN included the IELTS service fee income in ECAN’s taxable income and paid the tax, but did not register for value-added tax.

Income tax is levied on any taxable income received by an organization. As a result, if the amount of income tax is not included in the goods and services that are tax free under Schedule 1 of the Value Added Tax Act, 2052, the value added tax is also imposed. As the service charge for ECAN’s IELTS exceeds the threshold, it has been deemed that tax would be imposed.

Based on the income generated from the service charge imposed by ECAN, amounting to 66,188,842, it has been noted that there will be an increase in the threshold for taxation beyond 10 million. Consequently, it has been indicated that there will be an imposition of a tax increment based on this criterion.

Furthermore, in accordance with the same basis, the determined amount exceeding the threshold, 66,188,842, will be considered for tax assessment, resulting in a determination of 7,499,509 as per the prevailing law. Additionally, a decision was made by the office to impose an additional 10% tax, 15% interest, and a 100% penalty as per the same law.

After all these calculations, ECAN had set aside a total of 2,25,64,470 to be budgeted over six fiscal years.

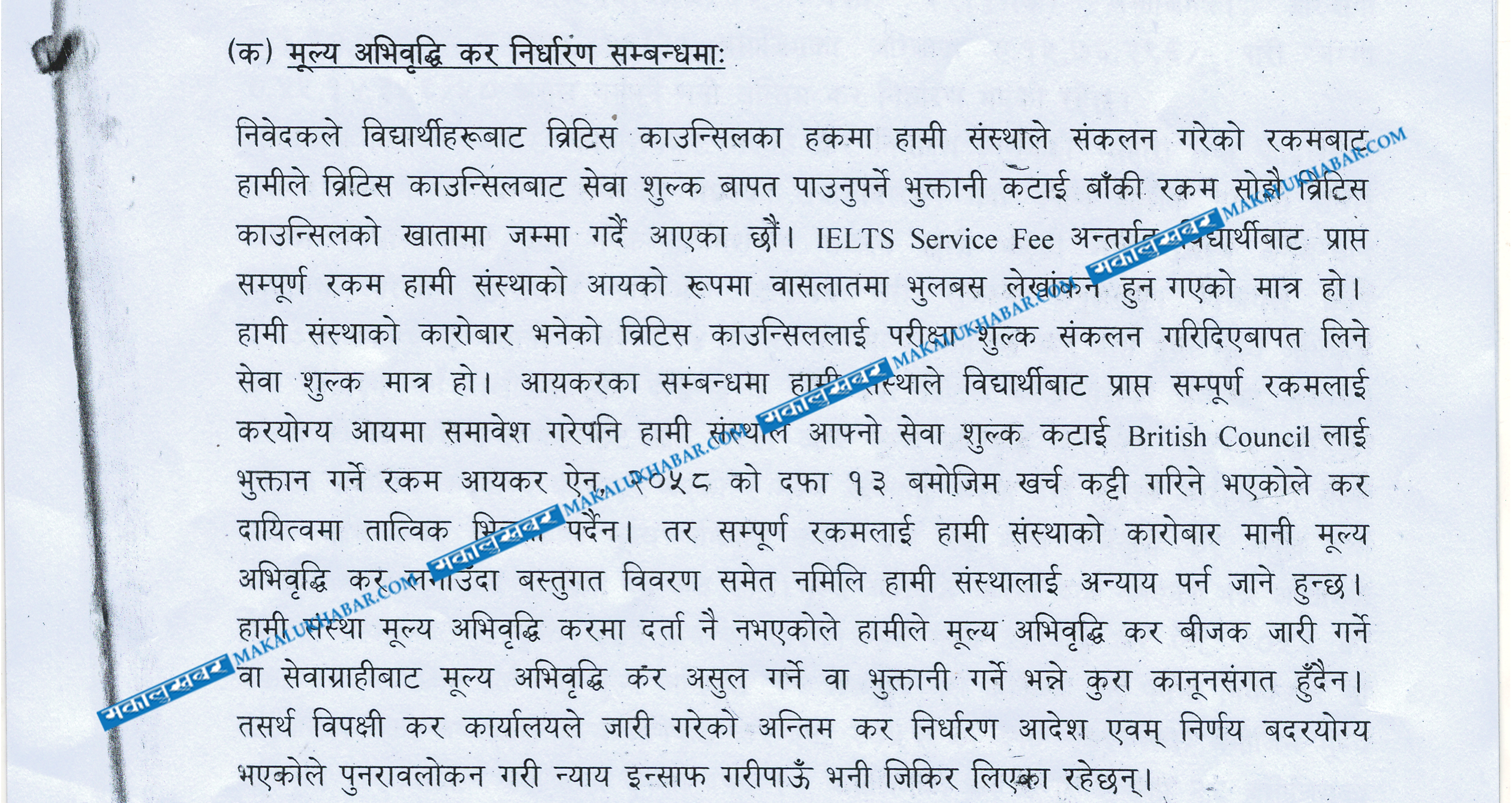

ECAN’s claim – we are not registered for value-added tax, we don’t have to pay

However, ECAN has claimed that it is not required to pay value added tax. Following the Revenue Office’s decision to pay with Value Added Tax, ECAN filed an appeal with the Revenue Department.

It has been reported that the educational consultants withdrew the money due from the British Council for the service charge from the amount collected from students on behalf of the British Council and paid the remainder straight into the British Council’s account.

ECAN’s answer is that the entire amount received from the students under the IELTS service fee has been wrongly written in the balance sheet as income of the institutions. ECAN has claimed that the business of the institutions is only a service fee for collecting examination fees from the British Council.

In regards to income tax, institutions have contended that despite the entirety of the students’ payments being accounted for in taxable income, there is no alteration in tax liability, given that the amount remitted to the British Council is subtracted from their service fees. However, ECAN stated that if the entire sum is regarded as the organization’s business and subjected to value-added tax, it would not only fail to align with the intended objectives but also result in unfair treatment of the organization.

Similarly, it has been asserted that as educational consultancy organizations are not registered for value-added tax, the issuance, collection, or payment of value-added tax from service users is not in compliance with the law.

Presenting these arguments, ECAN urged the relevant authorities to revoke the final tax assessment order issued by the tax office. However, the Revenue Tribunal affirmed the tax office’s directive to pay the value-added tax, and ECAN has resolved to comply with the requirement to settle the aforementioned tax.